GFD: GPU Fractional Differencing¶

![]()

Summary¶

Typically we attempt to achieve some form of stationarity via a transformation on our time series through common methods including integer differencing. However, integer differencing unnecessarily removes too much memory to achieve stationarity. An alternative, fractional differencing, allows us to achieve stationarity while maintaining the maximum amount of memory compared to integer differencing. While existing CPU-based implementations are inefficient for running fractional differencing on many large-scale time series, our GPU-based implementation enables rapid fractional differencing.

This tutorial walks you through our GPU implementation of fractional differencing (GFD). Also, this tutorial is a special collaboration between industry and academia led by me.

Credits¶

Before we start, I would like to thank and give credits for this particular post to: 1. NVIDIA (Ettikan, Chris and Nick), Amazon AWS, ensemblecap.ai, and NExT++ (NUS School of Computing) 2. Marcos Lopez de Prado for his recent push on the use of fractional differencing of which this guide is based on. 3. Hosking for his paper in 1981 on fractional differencing.

Links¶

- Code Repository: https://github.com/ritchieng/fractional_differencing_gpu

- Presentation: https://www.researchgate.net/publication/335159299_GFD_GPU_Fractional_Differencing_for_Rapid_Large-scale_Stationarizing_of_Time_Series_Data_while_Minimizing_Memory_Loss

Installation of Libraries (Optional)¶

- These steps are for easily running RAPIDS in Google Colab. You can skip this section if you've RAPIDS installed.

import pynvml

pynvml.nvmlInit()

handle = pynvml.nvmlDeviceGetHandleByIndex(0)

device_name = pynvml.nvmlDeviceGetName(handle)

print(f'Currently running on {device_name}')

if device_name != b'Tesla T4':

raise Exception("""

Unfortunately this instance does not have a T4 GPU.

Please make sure you've configured Colab to request a GPU instance type.

Sometimes Colab allocates a Tesla K80 instead of a T4. Resetting the instance.

If you get a K80 GPU, try Runtime -> Reset all runtimes -> Keep trying!

""")

else:

print('Woo! You got the right kind of GPU, a Tesla T4!')

Currently running on b'Tesla T4'

Woo! You got the right kind of GPU, a Tesla T4!

# intall miniconda

!wget -c https://repo.continuum.io/miniconda/Miniconda3-4.5.4-Linux-x86_64.sh

!chmod +x Miniconda3-4.5.4-Linux-x86_64.sh

!bash ./Miniconda3-4.5.4-Linux-x86_64.sh -b -f -p /usr/local

# install RAPIDS packages

!conda install -q -y --prefix /usr/local -c conda-forge \

-c rapidsai-nightly/label/cuda10.0 -c nvidia/label/cuda10.0 \

cudf cuml

# set environment vars

import sys, os, shutil

sys.path.append('/usr/local/lib/python3.6/site-packages/')

os.environ['NUMBAPRO_NVVM'] = '/usr/local/cuda/nvvm/lib64/libnvvm.so'

os.environ['NUMBAPRO_LIBDEVICE'] = '/usr/local/cuda/nvvm/libdevice/'

# copy .so files to current working dir

for fn in ['libcudf.so', 'librmm.so']:

shutil.copy('/usr/local/lib/'+fn, os.getcwd())

--2019-08-19 05:36:25-- https://repo.continuum.io/miniconda/Miniconda3-4.5.4-Linux-x86_64.sh

Resolving repo.continuum.io (repo.continuum.io)... 104.18.200.79, 104.18.201.79, 2606:4700::6812:c84f, ...

Connecting to repo.continuum.io (repo.continuum.io)|104.18.200.79|:443... connected.

HTTP request sent, awaiting response... 416 Requested Range Not Satisfiable

The file is already fully retrieved; nothing to do.

PREFIX=/usr/local

installing: python-3.6.5-hc3d631a_2 ...

Python 3.6.5 :: Anaconda, Inc.

installing: ca-certificates-2018.03.07-0 ...

installing: conda-env-2.6.0-h36134e3_1 ...

installing: libgcc-ng-7.2.0-hdf63c60_3 ...

installing: libstdcxx-ng-7.2.0-hdf63c60_3 ...

installing: libffi-3.2.1-hd88cf55_4 ...

installing: ncurses-6.1-hf484d3e_0 ...

installing: openssl-1.0.2o-h20670df_0 ...

installing: tk-8.6.7-hc745277_3 ...

installing: xz-5.2.4-h14c3975_4 ...

installing: yaml-0.1.7-had09818_2 ...

installing: zlib-1.2.11-ha838bed_2 ...

installing: libedit-3.1.20170329-h6b74fdf_2 ...

installing: readline-7.0-ha6073c6_4 ...

installing: sqlite-3.23.1-he433501_0 ...

installing: asn1crypto-0.24.0-py36_0 ...

installing: certifi-2018.4.16-py36_0 ...

installing: chardet-3.0.4-py36h0f667ec_1 ...

installing: idna-2.6-py36h82fb2a8_1 ...

installing: pycosat-0.6.3-py36h0a5515d_0 ...

installing: pycparser-2.18-py36hf9f622e_1 ...

installing: pysocks-1.6.8-py36_0 ...

installing: ruamel_yaml-0.15.37-py36h14c3975_2 ...

installing: six-1.11.0-py36h372c433_1 ...

installing: cffi-1.11.5-py36h9745a5d_0 ...

installing: setuptools-39.2.0-py36_0 ...

installing: cryptography-2.2.2-py36h14c3975_0 ...

installing: wheel-0.31.1-py36_0 ...

installing: pip-10.0.1-py36_0 ...

installing: pyopenssl-18.0.0-py36_0 ...

installing: urllib3-1.22-py36hbe7ace6_0 ...

installing: requests-2.18.4-py36he2e5f8d_1 ...

installing: conda-4.5.4-py36_0 ...

unlinking: ca-certificates-2019.6.16-hecc5488_0

unlinking: certifi-2019.6.16-py36_1

unlinking: conda-4.7.11-py36_0

unlinking: cryptography-2.7-py36h72c5cf5_0

unlinking: libgcc-ng-9.1.0-hdf63c60_0

unlinking: libstdcxx-ng-9.1.0-hdf63c60_0

unlinking: openssl-1.1.1c-h516909a_0

unlinking: python-3.6.7-h381d211_1004

unlinking: sqlite-3.28.0-h8b20d00_0

unlinking: tk-8.6.9-hed695b0_1002

installation finished.

WARNING:

You currently have a PYTHONPATH environment variable set. This may cause

unexpected behavior when running the Python interpreter in Miniconda3.

For best results, please verify that your PYTHONPATH only points to

directories of packages that are compatible with the Python interpreter

in Miniconda3: /usr/local

Solving environment: ...working... done

## Package Plan ##

environment location: /usr/local

added / updated specs:

- cudf

- cuml

The following packages will be UPDATED:

ca-certificates: 2018.03.07-0 --> 2019.6.16-hecc5488_0 conda-forge

certifi: 2018.4.16-py36_0 --> 2019.6.16-py36_1 conda-forge

conda: 4.5.4-py36_0 --> 4.7.11-py36_0 conda-forge

cryptography: 2.2.2-py36h14c3975_0 --> 2.7-py36h72c5cf5_0 conda-forge

libgcc-ng: 7.2.0-hdf63c60_3 --> 9.1.0-hdf63c60_0

libstdcxx-ng: 7.2.0-hdf63c60_3 --> 9.1.0-hdf63c60_0

openssl: 1.0.2o-h20670df_0 --> 1.1.1c-h516909a_0 conda-forge

python: 3.6.5-hc3d631a_2 --> 3.6.7-h381d211_1004 conda-forge

sqlite: 3.23.1-he433501_0 --> 3.28.0-h8b20d00_0 conda-forge

tk: 8.6.7-hc745277_3 --> 8.6.9-hed695b0_1002 conda-forge

Preparing transaction: ...working... done

Verifying transaction: ...working... done

Executing transaction: ...working... done

You would need to do a Runtime > Restart and Run All on your Google Colab notebook at this step.

Imports¶

# Critical imports for GPU cuDF

import nvstrings, nvcategory, cudf

# Other imports

import numpy as np

import pandas as pd

import time

import pandas_datareader.data as web

from datetime import datetime

from matplotlib import pyplot as plt

from numba import cuda

Plotting Style¶

# Display settings: just to make it slightly prettier

# There'll be a separate post on beautiful plots

%matplotlib inline

figsize=(25, 6)

plt.style.use('fivethirtyeight')

Necessity of Fractional Differencing¶

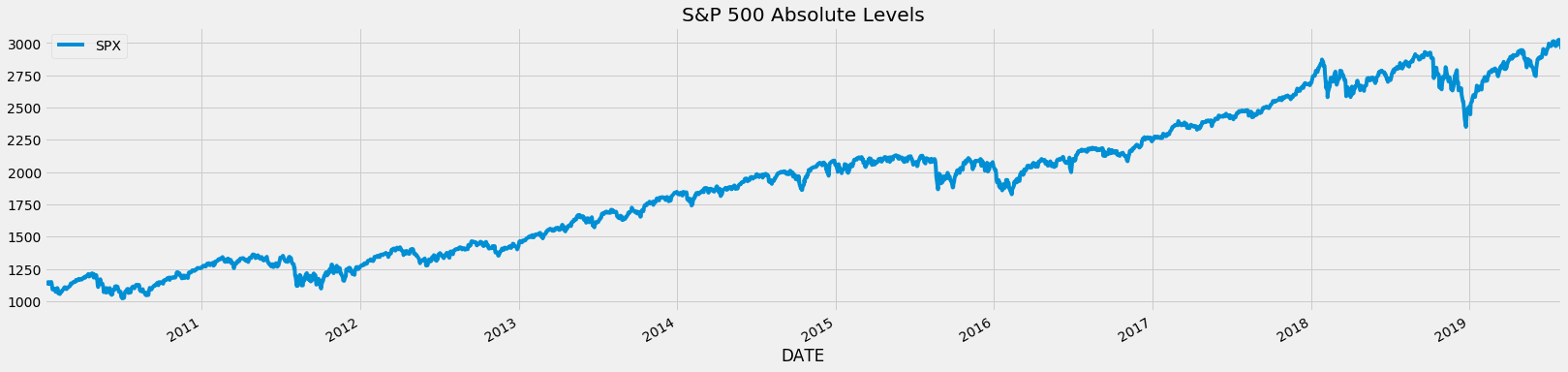

- Before we get into why fractional differencing is critical, let us inspect a simple time series pulled from the Fed's database: S&P 500.

Pulling, Processing & Plotting SPX Time Series¶

# Read SPX data 2010-2019 from FED database: https://fred.stlouisfed.org/categories/94

asset_name = 'SPX'

start = datetime(2010, 1, 1)

end = datetime(2019, 8, 1)

df_raw = web.DataReader('SP500', 'fred', start, end)

# Basic clean up data: dropna (there are other more robust treatments)

df_raw = df_raw.dropna()

df_raw.columns = [asset_name]

df_raw.plot(figsize=figsize)

plt.title('S&P 500 Absolute Levels');

Integer Differencing (1 Day Returns) SPX Time Series¶

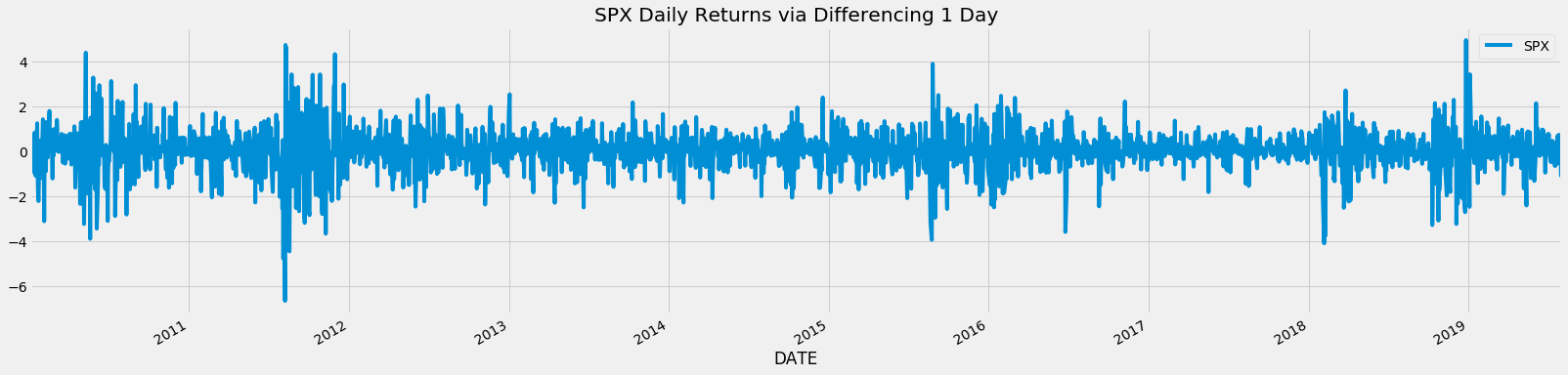

- Traditionally we typically might difference our time series by one day (daily returns) or more to reach some form of stationarity via tests like ADF, KPSS, PP and more.

- However, these forms of integer differencing causes more information than needed to be lost.

# One day returns calculation through differencing by 1

differencing_factor = 1

df_daily_returns = (df_raw - df_raw.shift(differencing_factor)) / df_raw.shift(differencing_factor) * 100

df_daily_returns.plot(figsize=figsize)

plt.title(f'{asset_name} Daily Returns via Differencing 1 Day');

Integer Differencing Causes Unnecessary Memory Loss¶

- Because of this reason, we propose fractional differencing to achieve stationarity while minimizing memory loss.

Basic Fractional Differencing¶

Fractional differencing allows us to achieve stationarity while maintaining the maximum amount of memory compared to integer differencing.

This was originally introduced in 1981 in his paper “Fractional Differencing” by J. R. M. Hosking1 and subsequent work by others concentrated on fast and efficient implementations for fractional differentiation for continuous stochastic processes. Recently, fractional differencing was introduced for financial time series through the fixed window fractional differencing instead of the expanding window method by Marcos Lopez de Prado2.

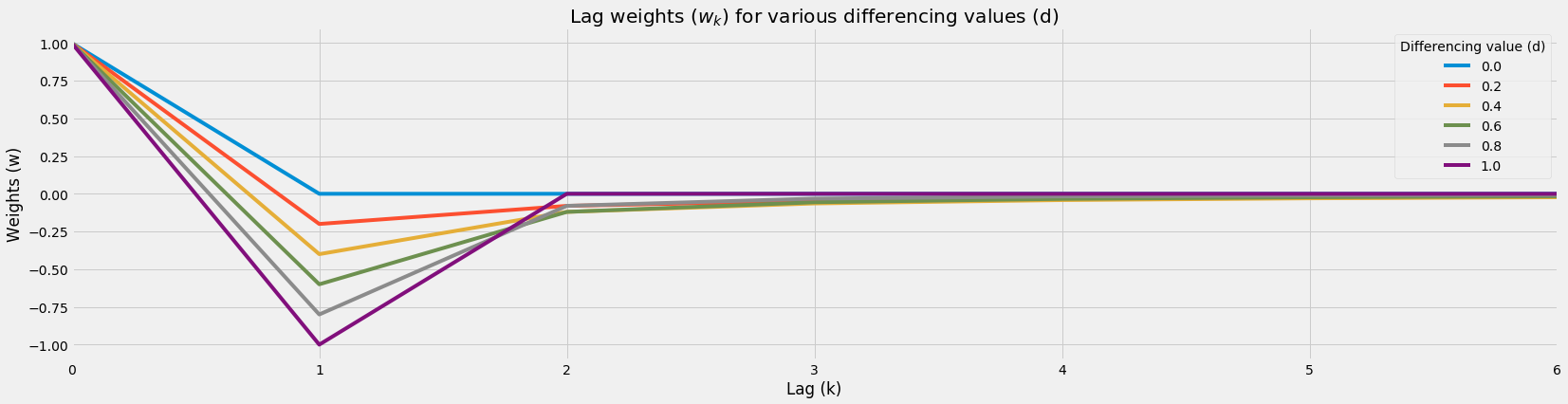

Fractional Differencing Weight Function and Plot¶

- Weights formula: \(w_k = -w_{k-1} \frac{d - k + 1}{k}\)

- Weight converges to zero: \(w_k \rightarrow 0\)

def get_weights(d, num_k):

r"""Calculate weights ($w$) for each lag ($k$) through

$w_k = -w_{k-1} \frac{d - k + 1}{k}$.

Args:

d (int): differencing value.

num_k (int): number of lags (typically length of timeseries) to calculate w.

"""

w_k = np.array([1])

for k in range(1, num_k):

w_k = np.append(w_k, -w_k[-1] * ((d - k + 1)) / k)

w_k = w_k.reshape(-1, 1)

return w_k

def plot_weights(range_d, num_k, num_d_interval):

r"""Plot weights ($w$) for each lag ($k$) for varying differencing value ($d$).

Args:

range_d (list): range of differencing values to plot.

num_k (int): number of lags (typically length of timeseries) to plot.

num_d_interval (int): number of d interval.

"""

# Get differencing values

interval = np.linspace(range_d[0], range_d[1], num_d_interval)

# Dataframe of lags (rows) x number of differencing intervals (columns)

df_wk = pd.DataFrame(np.zeros((num_k, num_d_interval)))

# Get weights array per differencing value

for i, d in enumerate(interval):

df_wk[i] = get_weights(d, num_k)

# Rename columns for legend

df_wk.columns = [round(x, 1) for x in interval]

# Plot

df_wk.plot(figsize=figsize)

plt.title('Lag weights ($w_k$) for various differencing values (d)')

plt.legend(title='Differencing value (d)')

plt.ylabel('Weights (w)')

plt.xlabel('Lag (k)')

plt.show()

# Return weights

return df_wk

df_wk = plot_weights(range_d=[0, 1], num_k=7, num_d_interval=6)

Fractional Differencing Weight Function Table¶

# Dataframe for lag weights (w) for various differencing values (d)

df_wk

| 0.0 | 0.2 | 0.4 | 0.6 | 0.8 | 1.0 | |

|---|---|---|---|---|---|---|

| 0 | 1.0 | 1.000000 | 1.000000 | 1.000000 | 1.000000 | 1.0 |

| 1 | -0.0 | -0.200000 | -0.400000 | -0.600000 | -0.800000 | -1.0 |

| 2 | -0.0 | -0.080000 | -0.120000 | -0.120000 | -0.080000 | 0.0 |

| 3 | -0.0 | -0.048000 | -0.064000 | -0.056000 | -0.032000 | 0.0 |

| 4 | -0.0 | -0.033600 | -0.041600 | -0.033600 | -0.017600 | 0.0 |

| 5 | -0.0 | -0.025536 | -0.029952 | -0.022848 | -0.011264 | 0.0 |

| 6 | -0.0 | -0.020429 | -0.022963 | -0.016755 | -0.007885 | 0.0 |

Fractional Differencing Value Calculation Toy Example¶

- Assume spot have values 100, 99, 98, 97, 96, 95, 94 from k=0 to k=6

For \(d = 0\) (no differencing)¶

differenced_value = 100 * 1 + 99 * 0 + 98 * 0 + 97 * 0 + 96 * 0 + 95 * 0 + 94 * 0

print(f'Differenced value: {differenced_value}')

df_wk.iloc[:, 0]

Differenced value: 100

0 1.0

1 -0.0

2 -0.0

3 -0.0

4 -0.0

5 -0.0

6 -0.0

Name: 0.0, dtype: float64

For \(d = 0.4\) (fractional differencing)¶

differenced_value = 100 * 1 + 99 * -0.400000 + 98 * -0.120000 + 97 * -0.064000 + 96 * -0.041600 + 95 * -0.041600 + 94 * -0.041600

print(f'Differenced value: {differenced_value}')

df_wk.iloc[:, 1]

Differenced value: 30.576000000000004

0 1.000000

1 -0.200000

2 -0.080000

3 -0.048000

4 -0.033600

5 -0.025536

6 -0.020429

Name: 0.2, dtype: float64

For \(d = 1\) (integer differencing)¶

differenced_value = 100 * 1 + 99 * -1 + 98 * 0 + 97 * 0 + 96 * 0 + 95 * 0 + 94 * 0

print(f'Differenced value: {differenced_value}')

df_wk.iloc[:, -1]

Differenced value: 1

0 1.0

1 -1.0

2 0.0

3 0.0

4 0.0

5 0.0

6 0.0

Name: 1.0, dtype: float64

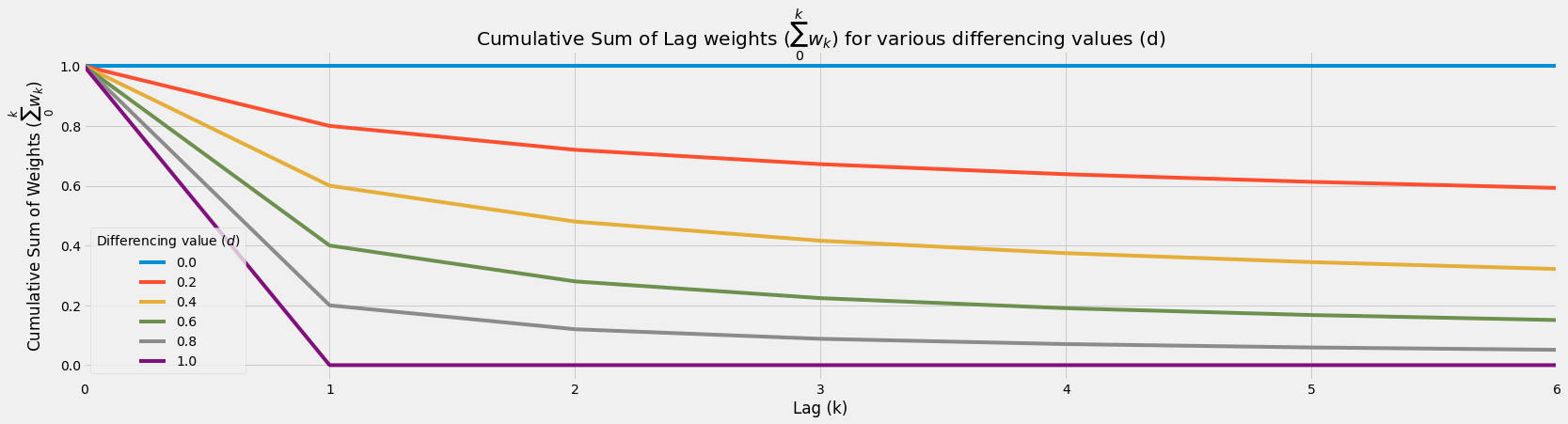

Cumulative Sum of Weights Behavior¶

- Higher differencing value would accelerate cumulative sum weight decay

- This causes:

- Less information taken from further lags

- More information loss from further lags

df_wk.cumsum().plot(figsize=figsize)

plt.title('Cumulative Sum of Lag weights ($\sum_0^k w_k$) for various differencing values (d)')

plt.legend(title='Differencing value ($d$)')

plt.ylabel('Cumulative Sum of Weights ($\sum_0^k w_k$)')

plt.xlabel('Lag (k)');

Fixed Window Fractional Differencing (CPU)¶

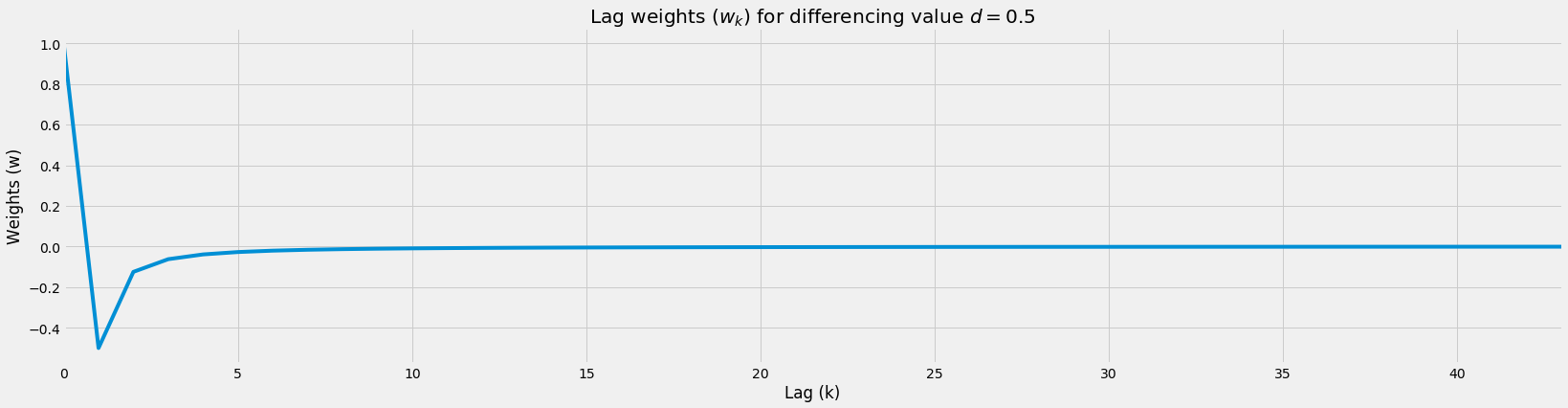

Floored Weights Function¶

- For computational efficiency, we want to stop the calculation of weights when the weights are too small (below a certain small predetermined small value).

- Image we had a time series with 1,000,000 data points, we do not want to compute the weights up till 1m lag for our latest data point!

- We can simply calculate the weights till they're too small which is what this function does.

def get_weights_floored(d, num_k, floor=1e-3):

r"""Calculate weights ($w$) for each lag ($k$) through

$w_k = -w_{k-1} \frac{d - k + 1}{k}$ provided weight above a minimum value

(floor) for the weights to prevent computation of weights for the entire

time series.

Args:

d (int): differencing value.

num_k (int): number of lags (typically length of timeseries) to calculate w.

floor (float): minimum value for the weights for computational efficiency.

"""

w_k = np.array([1])

k = 1

while k < num_k:

w_k_latest = -w_k[-1] * ((d - k + 1)) / k

if abs(w_k_latest) <= floor:

break

w_k = np.append(w_k, w_k_latest)

k += 1

w_k = w_k.reshape(-1, 1)

return w_k

# Show large time series being stopped

# Notice how max lag is at 9?

d = 0.5

num_k = 1000

weights = get_weights_floored(d=d, num_k=num_k)

pd.DataFrame(weights).plot(legend=False, figsize=figsize)

# Plot

plt.title(f'Lag weights ($w_k$) for differencing value $d={d}$')

plt.ylabel('Weights (w)')

plt.xlabel('Lag (k)');

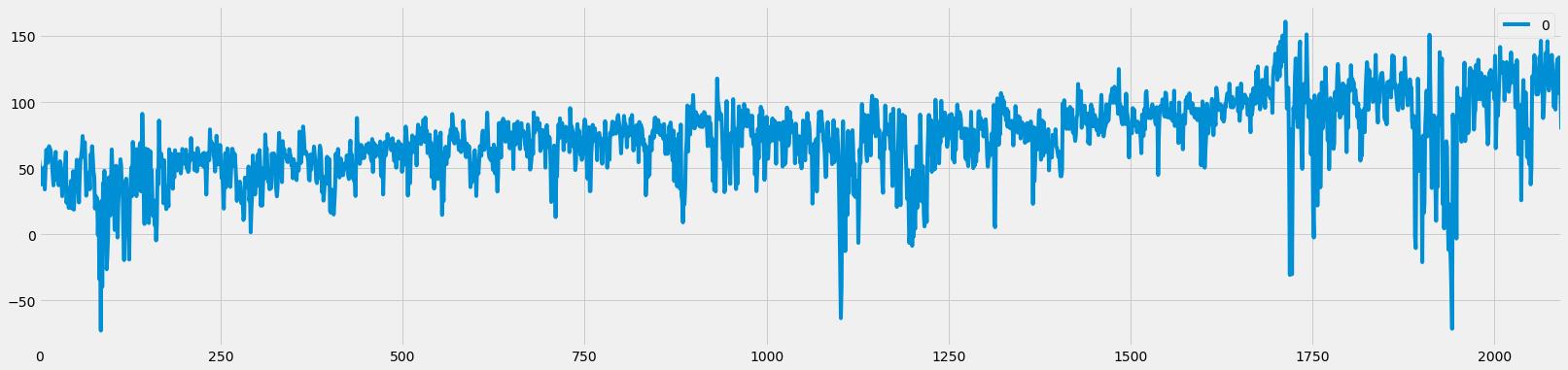

Fixed Window Fractional Differencing Function (CPU)¶

- Here, we use the new floored weights function compared to our normal weights function

- Calculate our differenced values through the dot product of our transposed weights matrix and our original time series within that window

- Keep repeating by shifting the window by one time step until the end of the time series

def frac_diff(df, d, floor=1e-3):

r"""Fractionally difference time series via CPU.

Args:

df (pd.DataFrame): dataframe of raw time series values.

d (float): differencing value from 0 to 1 where > 1 has no FD.

floor (float): minimum value of weights, ignoring anything smaller.

"""

# Get weights window

weights = get_weights_floored(d=d, num_k=len(df), floor=floor)

weights_window_size = len(weights)

# Reverse weights

weights = weights[::-1]

# Blank fractionally differenced series to be filled

df_fd = []

# Slide window of time series, to calculated fractionally differenced values

# per window

for idx in range(weights_window_size, df.shape[0]):

# Dot product of weights and original values

# to get fractionally differenced values

date_idx = df.index[idx]

df_fd.append(np.dot(weights.T, df.iloc[idx - weights_window_size:idx]).item())

# Return FD values and weights

df_fd = pd.DataFrame(df_fd)

return df_fd, weights

# Start timer

start = time.time()

df_raw_fd, weights = frac_diff(df_raw, d=0.5, floor=5e-5)

# End timer

end = time.time()

print(f'Time {end-start} s')

# Plot

df_raw_fd.plot(figsize=figsize);

Time 0.5417799949645996 s

import multiprocessing

multiprocessing.cpu_count()

4

Existing CPU-based implementations are inefficient for running fractional differencing on many large-scale time-series. GPU-based implementations provide an avenue to adapt to this century’s big data requirements.

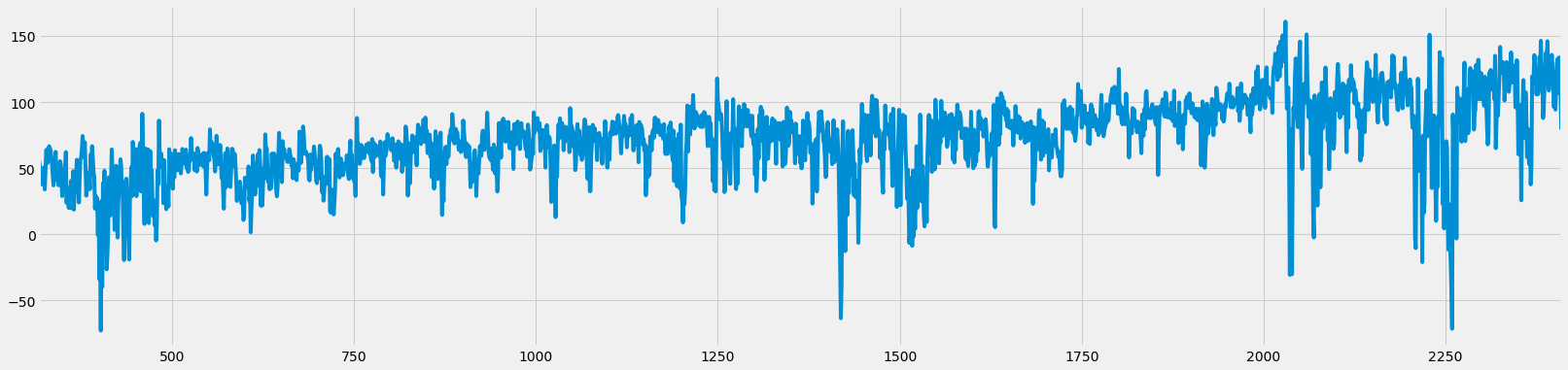

Fixed Window Fractional Differencing Function (GPU)¶

- This gives a slight 1.5x to 2x speed-up on an NVIDIA T4 on Google Colab for this tiny dataset

- For larger time series in line with real-world situations, it can easily be up to 100x to 1000x dataset (shown below).

def moving_dot_product_kernel(in_data, out, window_size, weights):

# Set the first window_size-1 rows in each chunk to np.nan due

# insufficient history

for i in range(cuda.threadIdx.x, window_size - 1, cuda.blockDim.x):

out[i] = np.nan

# Compute dot product of preceding window_size rows

for i in range(cuda.threadIdx.x + window_size - 1, in_data.size, cuda.blockDim.x):

rolling_dot_product = 0.0

k = 0

for j in range(i - window_size + 1, i + 1):

rolling_dot_product += in_data[j] * weights[k][0]

k += 1

out[i] = rolling_dot_product

def frac_diff_gpu(df, d, floor=1e-3):

r"""Fractionally difference time series via GPU.

Args:

df (pd.DataFrame): dataframe of raw time series values.

d (float): differencing value from 0 to 1 where > 1 has no FD.

floor (float): minimum value of weights, ignoring anything smaller.

"""

# Bring dataframe to GPU, reset index for GPU dot product kernel

gdf_raw = cudf.from_pandas(df).reset_index(drop=True)

gdf_raw.columns = ['in_data']

# Get weights window

weights = get_weights_floored(d=d, num_k=len(gdf_raw), floor=floor)

weights_window_size = len(weights)

# Reverse weights and as contiguous

weights = np.ascontiguousarray(weights[::-1])

# Bring weights to GPU

gdf_weights = cudf.DataFrame()

gdf_weights[gdf_raw.columns[0]] = weights.reshape(-1)

# Length of data

data_length = len(gdf_raw)

# T4: max of 518 threads per block.

# V100: max 1024 threads per block

threads_per_block = 518

# Chunk size split

# This has to be improved, but as a v0.1, it's sufficient to show speed-up

# Up to easily 100 million data points

trunk_size = data_length

# Get fractionally differenced time series through GPU function

gdf_raw_fd = gdf_raw.apply_chunks(moving_dot_product_kernel,

incols=['in_data'],

outcols=dict(out=np.float64),

kwargs=dict(window_size=weights_window_size, weights=weights),

chunks=list(range(0, data_length, trunk_size)) + [data_length],

tpb=threads_per_block)

# Bring to CPU for normal manipulation

df_raw_fd = gdf_raw_fd.to_pandas().dropna().iloc[:-1, 1]

return df_raw_fd, weights

# Start timer

start = time.time()

df_raw_fd_from_gpu, weights = frac_diff_gpu(df_raw, d=0.5, floor=5e-5)

# End timer

end = time.time()

print(f'Time {end-start} s')

# Plot

df_raw_fd_from_gpu.plot(figsize=figsize);

Time 0.27262187004089355 s

Check Values¶

# Compare tail values

print('Tail values check')

print(df_raw_fd_from_gpu.tail().values)

print(df_raw_fd.tail().values.reshape(-1,))

Tail values check

[107.00340988 133.85520208 117.92878691 109.44132697 79.32562638]

[107.00340988 133.85520208 117.92878691 109.44132697 79.32562638]

# Compare tail values

print('Head values check')

print(df_raw_fd_from_gpu.head().values)

print(df_raw_fd.head().values.reshape(-1,))

Head values check

[56.74989213 52.56766288 47.32421832 45.89772154 37.74401501]

[56.74989213 52.56766288 47.32421832 45.89772154 37.74401501]

num_rows_true = (df_raw_fd.values.astype(np.float32) == df_raw_fd_from_gpu.values.astype(np.float32)).astype(int).sum()

total_rows = df_raw_fd.shape[0]

print(f'Number of rows equal: {num_rows_true}')

print(f'Total number of rows: {total_rows}')

Number of rows equal: 2093

Total number of rows: 2093

Stationarity¶

- "A stationary time series is one whose statistical properties such as mean, variance, autocorrelation, etc. are all constant over time", Robert Nau, Duke University

- Essentially what we are trying to do here with fractional differencing is to attempt to have a stationary time series without losing too much memory.

- There are many ways to check if a time series is stationary, but we will be using 1 test here (they're more, but it's not the purpose of this tutorial)

- Augmented Dickey–Fuller (ADF) test: check for unit root

ADF Test¶

# Import adf/kpss

from statsmodels.tsa.stattools import adfuller

import warnings

warnings.filterwarnings("ignore") # Ignore deprecations for cleaner output

ADF: raw data (d=0)¶

# ADF on raw data

print('Stationarity Test for SPX Absolute Levels (d=0)')

print('-'*50)

result = adfuller(df_raw['SPX'], regression='c')

print(f't-stat \n\t{result[0]:.2f}')

print(f'p-value \n\t{result[1]:.2f}')

print(f'Critical Values')

for key, value in result[4].items():

print(f'\t{key}: {value:.2f}')

# test statistic > test statistic (1%) AND p-value > 0.01

# Fail to reject the null hypothesis that there's unit root at the 1% significance level

# ==> Fail to reject H0 ==> Unit root ==> Non-stationary

Stationarity Test for SPX Absolute Levels (d=0)

--------------------------------------------------

t-stat

-0.11

p-value

0.95

Critical Values

1%: -3.43

5%: -2.86

10%: -2.57

ADF: daily return data (d=1)¶

# ADF on 1 day returns (d=1)

print('Stationarity Test for SPX Daily Returns (d=1)')

print('-'*50)

result = adfuller(df_raw['SPX'].pct_change(1).dropna(), regression='c')

print(f't-stat \n\t{result[0]:.2f}')

print(f'p-value \n\t{result[1]:.2f}')

print(f'Critical Values')

for key, value in result[4].items():

print(f'\t{key}: {value:.2f}')

# test statistic < test statistic (1%) AND p-value < 0.01

# Reject the null hypothesis that there's unit root at the 1% significance level

# ==> Reject H0 ==> No unit root ==> Stationary

Stationarity Test for SPX Daily Returns (d=1)

--------------------------------------------------

t-stat

-11.12

p-value

0.00

Critical Values

1%: -3.43

5%: -2.86

10%: -2.57

ADF: fractionally differenced data (d=0.5)¶

# ADF on fractionally differenced values

print('Stationarity Test (ADF) for SPX Fractionally Differenced (d=0.5)')

print('-'*50)

df_raw_fd_from_gpu, weights = frac_diff_gpu(df_raw, d=0.5, floor=5e-5)

result = adfuller(df_raw_fd_from_gpu, regression='c')

print(f't-stat \n\t{result[0]:.2f}')

print(f'p-value \n\t{result[1]:.2f}')

print(f'Critical Values')

for key, value in result[4].items():

print(f'\t{key}: {value:.2f}')

# test statistic < test statistic (1%) AND p-value < 0.01

# Reject the null hypothesis that there's unit root at the 1% significance level

# ==> Reject H0 ==> No unit root ==> Stationary

Stationarity Test (ADF) for SPX Fractionally Differenced (d=0.5)

--------------------------------------------------

t-stat

-3.86

p-value

0.00

Critical Values

1%: -3.43

5%: -2.86

10%: -2.57

Large-scale Rapid Fractional Differencing¶

- Here we test on a 100k, 1m, 10m and 100m datapoint dataframe.

# Create 100m data points

large_time_series_length = int(1e6)

print(large_time_series_length)

1000000

# Start timer

start = time.time()

df_raw = pd.DataFrame(np.arange(large_time_series_length) * np.random.rand(large_time_series_length))

df_raw_fd_from_gpu, weights = frac_diff_gpu(df_raw, d=0.5, floor=5e-5)

# End timer

end = time.time()

print(f'Time {end-start} s')

# Check

print('FD Shape', df_raw_fd_from_gpu.shape[0])

print('Correct Shape', df_raw.shape[0] - weights.shape[0])

print('Original Shape', df_raw.shape[0])

Time 0.4671785831451416 s

FD Shape 999682

Correct Shape 999682

Original Shape 1000000

# Start timer

start = time.time()

# Create 100m data points

df_raw = pd.DataFrame(np.arange(large_time_series_length) * np.random.rand(large_time_series_length))

df_raw_fd, weights = frac_diff(df_raw, d=0.5, floor=5e-5)

# End timer

end = time.time()

print(f'Time {end-start} s')

# Check

print('FD Shape', df_raw_fd_from_gpu.shape[0])

print('Correct Shape', df_raw.shape[0] - weights.shape[0])

print('Original Shape', df_raw.shape[0])

Time 128.29733324050903 s

FD Shape 999682

Correct Shape 999682

Original Shape 1000000